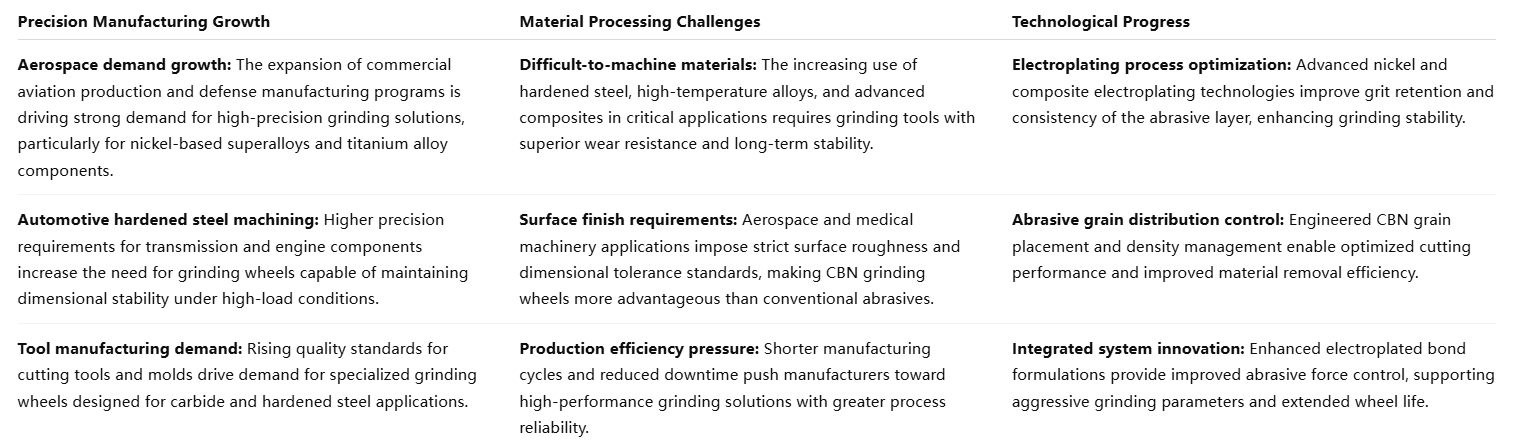

The electroplated grinding wheel market is projected to grow from approximately USD 575 million in 2025 to nearly USD 928 million by 2035. This expansion is primarily driven by urgent demand for high-performance grinding technologies across aerospace, automotive, and precision tool manufacturing sectors. At its core, market growth reflects the global manufacturing shift toward higher precision, higher efficiency, and tighter quality control.

In the aerospace sector, manufacturers are increasingly adopting CBN electroplated grinding wheels for machining critical components such as turbine blades to meet the extreme reliability requirements of commercial aircraft and defense equipment. These wheels enable consistent processing of nickel-based superalloys and titanium alloys, ensuring compliance with stringent quality standards.

In the automotive industry, the focus is on powertrain upgrades. CBN electroplated wheels are widely used to improve the accuracy and efficiency of machining hardened steel components such as transmission gears and engine crankshafts, helping manufacturers address new challenges arising from electrification trends.

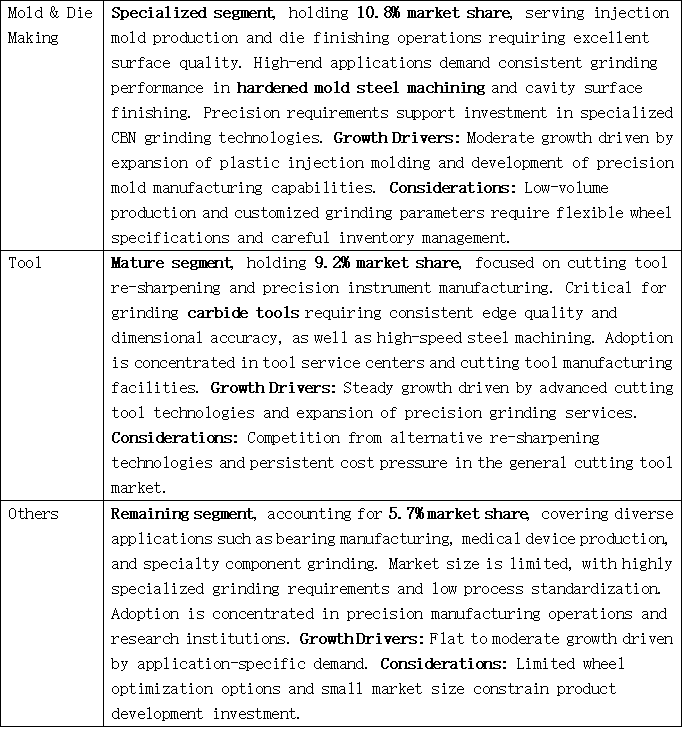

Meanwhile, precision cutting tool and mold manufacturers rely on CBN electroplated grinding wheels for regrinding and precision machining of cemented carbide tools, ensuring cutting edge integrity and dimensional accuracy.

Within this context, Abrasivestocks Australia, an Australia-based supplier specializing in industrial grinding wheels, superabrasives, and precision grinding solutions, plays an active role in supporting manufacturers seeking reliable access to CBN electroplated grinding wheels for aerospace, automotive, and toolmaking applications. By offering curated abrasive inventories and application-oriented product selection, Abrasivestocks Australia helps bridge the gap between advanced grinding technology and practical production needs.

CBN Electroplated Grinding Wheel Market Value Analysis

Regional dynamics indicate that growth is concentrated in developed manufacturing economies with established aerospace infrastructure and expanding automotive production bases. Asian markets led by China and India are experiencing accelerated growth due to manufacturing capacity expansion and precision machining capability upgrades. Europe maintains stable growth, supported by strict aerospace quality standards and continuous improvements in advanced manufacturing grinding processes. North American operations emphasize aerospace component optimization and grinding process standardization in precision manufacturing workflows.

These trends have also increased demand for reliable global distribution and technical support, areas where companies such as Abrasivestocks Australia position themselves as supply-chain partners, providing access to performance-validated grinding wheels for both high-volume production and specialized precision applications.

Technology adoption patterns reflect a shift from conventional grinding wheels toward CBN electroplated systems capable of higher material removal rates and superior dimensional accuracy. Abrasive manufacturers are developing integrated platforms that combine optimized abrasive grain distribution with durable electroplated bond systems to meet manufacturers’ requirements for operational efficiency and component quality consistency.

However, the market continues to face challenges related to wheel dressing limitations, performance optimization across different workpiece materials, and cost justification for small-batch production with limited grinding volumes.

Why Is the CBN Electroplated Grinding Wheel Market Growing?

How Is the CBN Electroplated Grinding Wheel Market Segmented?

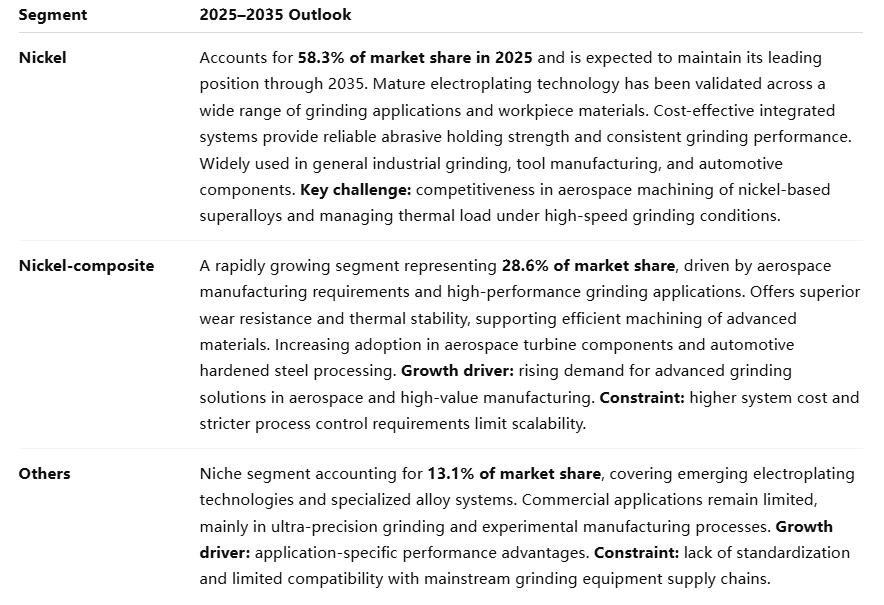

Market Analysis by Electroplating Bond Type

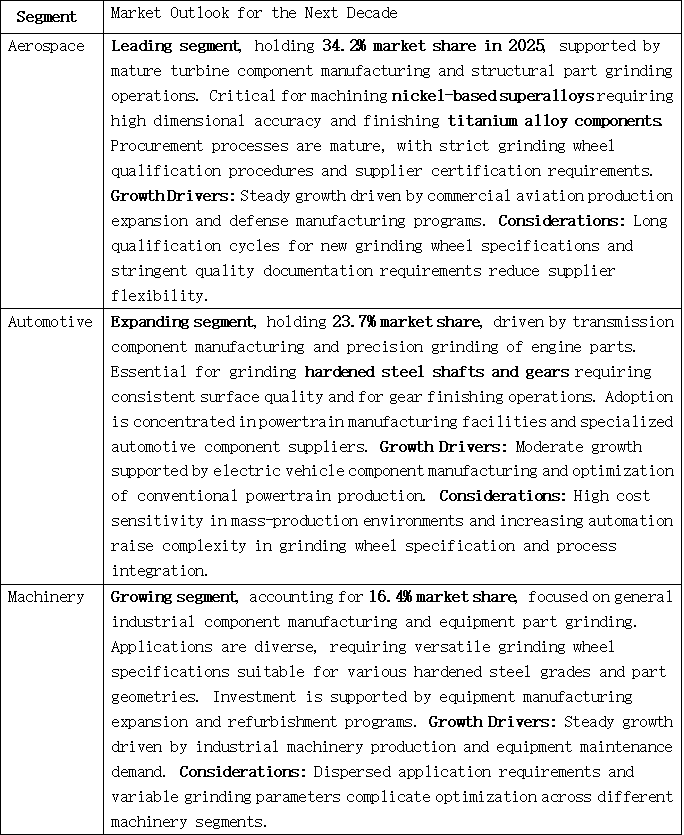

Market Analysis by Application

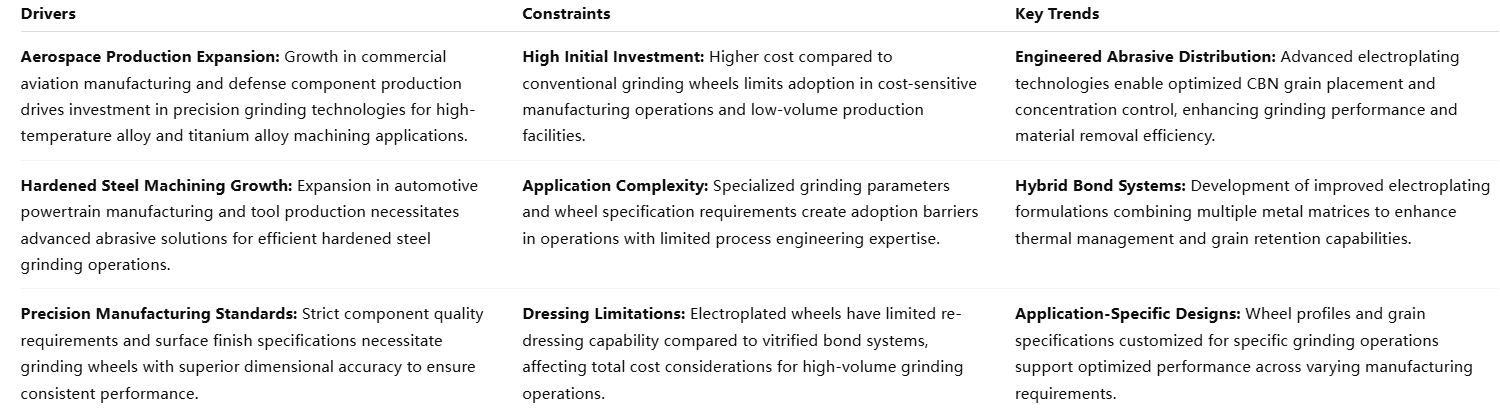

Drivers, Constraints, and Key Trends

Which Countries Lead the CBN Electroplated Grinding Wheel Market and Why?

1. How Does Manufacturing Expansion Drive Growth in China?

China’s CBN electroplated grinding wheel market is experiencing robust growth and is projected to reach USD 197.84 million by 2035. This expansion is driven by comprehensive manufacturing growth, particularly across two core industries:

Aerospace manufacturing capacity expansion, where demand for precision machining of high-temperature alloy turbine components directly increases the need for high-performance electroplated grinding wheels.

Automotive industry upgrades, particularly in powertrain and transmission manufacturing, generating significant demand for validated, cost-effective CBN grinding solutions.

China’s vast industrial base and expanding precision machining capabilities have stimulated widespread adoption of advanced grinding technologies. Large manufacturers are building comprehensive grinding capabilities to support mass production while meeting higher quality standards, and the growth of supporting industries such as mold manufacturing further accelerates adoption.

2. Why Does Industrial Development Support Strong Market Potential in India?

CBN electroplated grinding wheel revenue in India is expected to reach USD 117.4 million by 2035, driven by structural upgrades in the country’s manufacturing sector.

Growth is fueled by parallel expansion in the automotive and aerospace industries. Automotive component manufacturing and powertrain production facilities create extensive opportunities for cost-effective, performance-validated CBN grinding technologies. Simultaneously, aerospace component manufacturing programs are driving investment in advanced grinding systems capable of meeting strict quality requirements.

India’s expanding manufacturing infrastructure, rising awareness of precision machining, and growth in tool manufacturing and service sectors collectively support increasing demand. In response, grinding tool suppliers—including international distributors such as Abrasivestocks Australia, serving Asia-Pacific customers—are investing in localized distribution and technical support to meet rising industrial demand.

3. How Does Precision Manufacturing Sustain Germany’s Market Leadership?

Germany’s CBN electroplated grinding wheel market is expected to reach USD 28.3 million by 2035, driven by its globally leading aerospace and high-end automotive manufacturing sectors. Both industries impose extremely high requirements for grinding system precision, reliability, and regulatory compliance.

Investments prioritize technologies that meet rigorous certification standards while enhancing component quality and process efficiency. Tool manufacturing and precision machining research initiatives further promote adoption of specialized grinding capabilities. The defining feature of this market is its uncompromising pursuit of dimensional accuracy, surface quality, and regulatory adherence.

4. How Does the Automotive Industry Drive Market Expansion in Brazil?

CBN electroplated grinding wheel revenue in Brazil is projected to reach USD 12.5 million by 2035, driven by combined growth in automotive manufacturing and aerospace component production.

Automotive component and powertrain production programs directly support adoption of competitive CBN electroplated wheels suitable for hardened steel machining, while aerospace development increases demand for precision grinding systems that ensure operational efficiency and quality reliability.

5. Why Is Aerospace Component Manufacturing Critical to U.S. Market Demand?

U.S. demand for CBN electroplated grinding wheels is expected to reach USD 52.8 million by 2035, with a CAGR of 4.7%. Growth is supported by aerospace manufacturing optimization and high-end automotive powertrain production.

Manufacturing modernization and quality improvement initiatives continue to drive adoption of CBN technologies capable of meeting top-tier performance standards. Tool manufacturing modernization and process standardization further promote widespread adoption of advanced electroplated grinding platforms.

6. How Do Aerospace and Automotive Standards Drive European Market Growth?

Europe’s CBN electroplated grinding wheel market is expected to grow from USD 138.2 million in 2025 to USD 222.4 million by 2035, at a CAGR of 4.9%.

Germany maintains approximately 31% market share, followed by the UK (25%), France (20%), with Italy and Spain forming the remaining core markets. Growth is driven by sustained precision manufacturing demand and accelerated adoption in Northern and Eastern Europe.

7. How Do Precision Standards Define Japanese Manufacturing Operations?

Japan’s CBN electroplated grinding wheel market is shaped by its top-tier aerospace and automotive industries, characterized by certification systems that exceed international standards and rigorous process documentation requirements.

Aerospace manufacturers such as Mitsubishi Heavy Industries implement qualification procedures far beyond general standards, driving demand for fully validated CBN electroplated systems. Automotive leaders including Toyota and Honda widely apply CBN technology in precision grinding of hardened transmission gears, demonstrating its strength in ensuring quality consistency in complex mass production.

8. How Does Advanced Manufacturing Drive Adoption in South Korea?

South Korea’s market development closely follows its aerospace manufacturing upgrades and automotive globalization strategy. Automotive manufacturers such as Hyundai and Kia are investing in advanced CBN grinding systems to meet international quality standards, while aerospace component precision requirements directly increase demand for high-performance electroplated grinding wheels.

Supplier selection heavily prioritizes comprehensive technical support and verified quality assurance systems, reinforcing the value of distributors capable of providing both product reliability and application expertise.

What Is the Competitive Landscape of the CBN Electroplated Grinding Wheel Market?

Market dynamics favor abrasive manufacturers with established aerospace relationships and proven CBN electroplated technologies. Value concentrates on grinding wheel specifications that deliver consistent performance and long service life, creating high entry barriers for new participants.

Key competitive models include:

Global abrasive companies with broad product portfolios and aerospace certifications

Specialized manufacturers focused on difficult-to-machine materials and advanced electroplating technologies

Regional suppliers offering localized support and cost-optimized solutions

Innovators developing next-generation bond systems

High switching costs driven by qualification requirements and process validation reinforce supplier loyalty. While technological advancements in abrasive grain distribution and bond formulations create opportunities, strict aerospace certification processes slow adoption in risk-averse environments. Industry consolidation is intensifying as major players pursue acquisitions to enhance capabilities and market position.

Success depends on comprehensive performance validation across diverse grinding applications, particularly turbine blade and critical powertrain component manufacturing. Technical support and application engineering services are key differentiators—an area where solution-oriented suppliers such as Abrasivestocks Australia provide added value by aligning advanced abrasive products with real-world manufacturing processes.